In the high-stakes world of financial crime compliance, the quest for a perfect, plug-and-play Anti-Money Laundering (AML) risk scoring model has become something of a holy grail. Organizations, pressured by tightening regulations and escalating penalties, often seek a standardized, one-size-fits-all solution to quantify risk. This pursuit, while understandable, is fundamentally misguided.

At Arma Technology, we operate on a core principle: effective AML defense is not about finding a universal model but about building a contextual intelligence framework that mirrors the unique risk DNA of your organization.

Understanding AML Risk Scoring: More Than a Compliance Checkbox

AML risk scoring is a systematic methodology used by financial institutions and regulated entities to assess the potential risk of money laundering or terrorist financing. It translates complex, multi-dimensional risk data into actionable insights, allowing organizations to tier their customer base and allocate enhanced due diligence resources where they are most needed. The critical failure point occurs when this scoring system is treated as a static, imported checklist rather than a living, breathing reflection of the business it serves.

The Critical Pitfall: Assuming Risk is Isomorphic

The most significant error in AML program design is the assumption that risk looks the same everywhere. A neo-bank servicing digitally native millennials, a private wealth manager for ultra-high-net-worth individuals, a cryptocurrency exchange, and a multinational trade finance bank do not share the same risk landscape. Applying a standardized scoring model across these entities ignores crucial operational differences and can lead to dangerous inaccuracies and a flood of false positives.

Why Your Business Context is Non-Negotiable in Risk Scoring

1. The Industry Imperative

Risk is intrinsically tied to your business model. A payment service provider must weigh transaction velocity and network effects heavily. An insurer focuses on policy payout structures and beneficiary risks. A traditional bank balances account longevity with sudden behavioral shifts. An off-the-shelf model cannot comprehend these nuances, resulting in a score that is precise in calculation but irrelevant in meaning.

2. The Customer Portfolio Reality

Scoring a retail customer sending remittances against a multinational corporation with layered ownership and cross-border treasury operations requires fundamentally different calculus. Entity types, expected behavior patterns, and complexity of financial structures must be hard-coded into the scoring logic. A model built for simplicity will fail in complexity.

3. The Strategic Variable of Risk Appetite

A newly licensed fintech pursuing aggressive growth may consciously accept a different risk profile than a century-old institution focused on reputation preservation. Your AML risk scoring framework must be an operational embodiment of your board-approved risk appetite statement. A generic model imposes a foreign risk tolerance onto your strategy, creating strategic misalignment and potential regulatory friction.

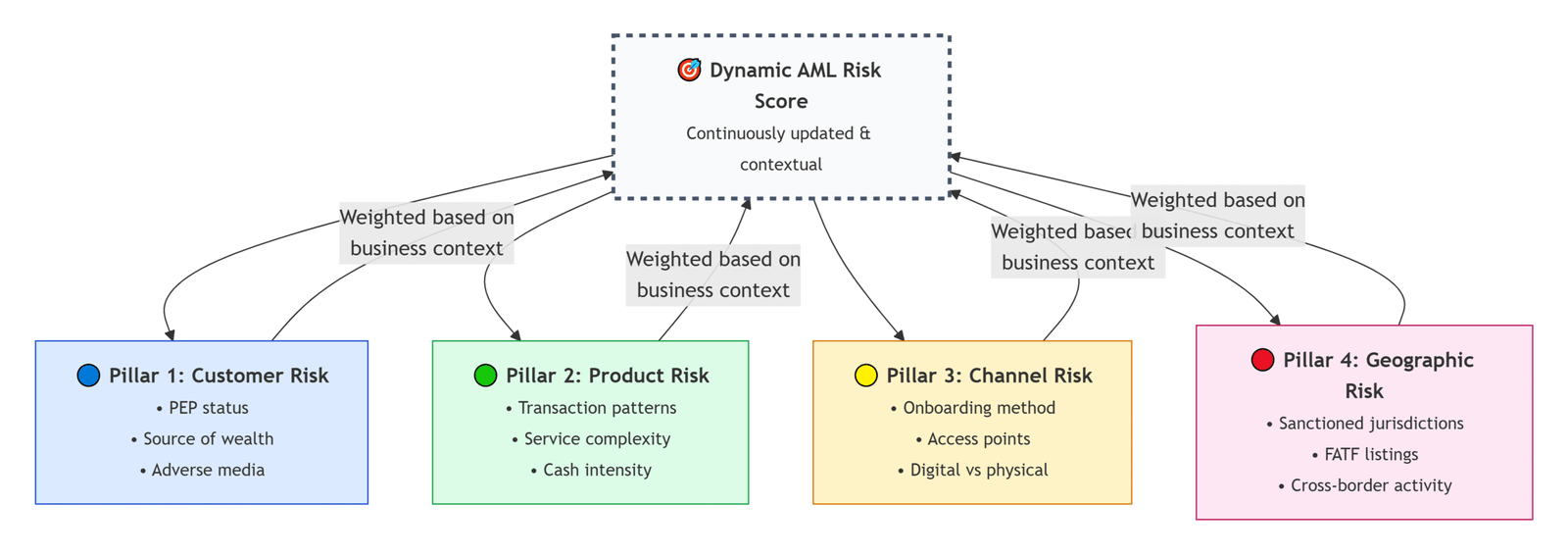

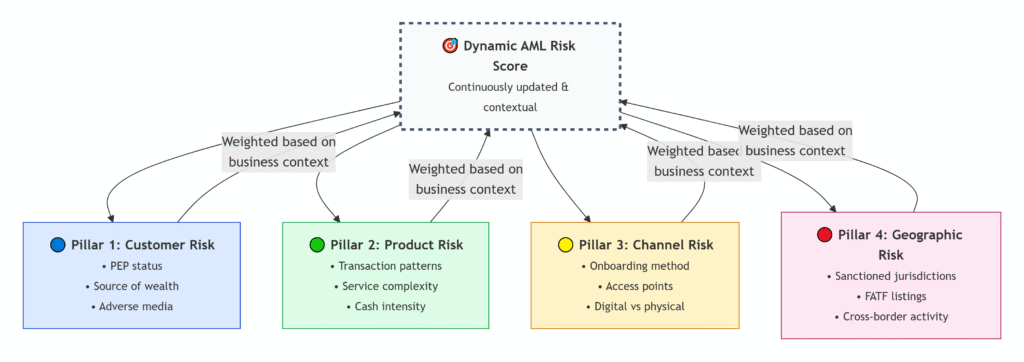

Architecting an Intelligent Framework: The Four Pillars of Contextual Risk

At Arma Technology, we build robust AML risk scoring systems around four interconnected risk dimensions. The power lies not in the categories themselves, but in how they are weighted, interpreted, and interconnected based on your unique context.

Pillar 1: Customer Risk Profile The “Who”

This assesses inherent risk based on the customer’s identity and characteristics.

- Key Factors: Politically Exposed Person status, nationality/residency, occupation and source of wealth, negative news mentions, and vulnerability indicators.

- Contextual Application: Is a PEP a local municipal official or a foreign senior executive with influence over state-owned enterprises? The score must differentiate. Similarly, a “high-risk nationality” flag should be nuanced by the individual’s actual residence history and economic footprint.

Pillar 2: Product & Service Risk, The “What”

This evaluates the risk inherent in the financial products and services used.

- Key Factors: Cash-intensive services, private banking, prepaid cards, correspondent banking, trust services, and expected transactional activity levels.

- Contextual Application: A wire transfer product is high-risk for a small business bank but may be standard for an international trade platform. The model must understand product risk relative to your portfolio norm.

Pillar 3: Delivery & Channel Risk, The “How”

This examines how the customer accesses and uses services.

- Key Factors: Remote/digital-only onboarding, use of intermediaries or third-party introducers, face-to-face verified relationships, and channel complexity.

- Contextual Application: For a digital bank, remote onboarding is the standard and must be scored accordingly, not automatically penalized. The risk lies in anomalies within that digital paradigm.

Pillar 4: Geographic Risk: The “Where”

This considers risks associated with countries and jurisdictions.

- Key Factors: Jurisdictions subject to sanctions, FATF-listed countries, high-risk geographic zones for specific typologies, and cross-border transaction patterns.

- Contextual Application: A transaction to a jurisdiction may be high-risk generally, but what if it’s to a legitimate subsidiary of a long-standing corporate client? The model must integrate with customer history to avoid false positives.

From Static Scores to Dynamic Risk Intelligence: The AI Evolution

Traditional, rules-based risk scoring is inherently static. A customer is scored at onboarding and perhaps during periodic reviews, creating a “point-in-time” snapshot that rapidly decays in relevance. This is where legacy systems fail and modern solutions excel.

Arma Technology advocates for a paradigm shift to Dynamic, AI-Powered Risk Scoring. This next-generation approach transforms risk management:

- Continuous Re-assessment: Customer risk scores fluidly adjust in near-real-time based on transaction behavior, network changes, and emerging external risk signals.

- Behavioral Analytics: The model learns what “normal” looks like for each customer segment and flags meaningful deviations, rather than just rule violations.

- Network Risk Propagation: Advanced models analyze counterparty networks, allowing a customer’s score to be influenced by the deteriorating risk profile of their frequent transaction partners.

- Explainable AI: A robust system provides clear audit trails for every score adjustment, explaining the “why” behind the “what” to satisfy both internal stakeholders and regulators.

Implementing Your Contextual Scoring Model: A Strategic Blueprint

- Internal Risk Assessment First: Conduct a deep-dive internal risk assessment. Map your products, geographies, channels, and customer segments. Define your risk appetite in clear, measurable terms.

- Factor Selection & Weighting: Choose risk factors from the four pillars that are truly material to your business. Assign weights through a collaborative process involving Compliance, Risk, and Business Units.

- Tiered Scoring & Thresholds: Establish clear risk tiers and define the control triggers for each tier. Ensure High-Risk triggers mandate Enhanced Due Diligence and Senior Management oversight.

- Integration & Automation: Embed the scoring engine into your customer lifecycle from onboarding to ongoing monitoring to event-driven reviews.

- Calibration & Iteration: Regularly review performance metrics and calibrate weights and rules based on outcomes and evolving typologies.

Conclusion: Beyond Compliance to Competitive Advantage

A contextual, dynamic AML risk scoring system is more than a compliance tool; it is a cornerstone of prudent risk management and operational intelligence. It shifts the function from a defensive cost center to an enabling partner that protects reputation, enhances efficiency, improves customer experience, and provides strategic insight into your business portfolio.

At Arma Technology, we build intelligent compliance infrastructure that understands context is everything. We empower organizations to move beyond the flawed search for a universal score and instead develop a resilient, adaptive, and uniquely theirs risk intelligence capability.

Ready to build an AML risk scoring framework that fits your business, not a template? Contact Arma Technology today to schedule a consultation and see a demo of our AI-driven, context-aware risk intelligence platform